Deposit Insurance: Is Your Money Safe in the Bank?

Are Your Deposits Insured? Understanding Deposit Insurance

Hello, how are you? Greetings! When it comes to safeguarding your hard-earned money, understanding whether your deposits are insured is crucial. Deposit insurance provides a safety net, ensuring that your funds remain protected even if your bank faces financial difficulties. Greetings again! This article will explore the essentials of deposit insurance, why it matters, and how you can verify the coverage of your accounts. Please continue reading.

What Is Deposit Insurance and How It Works

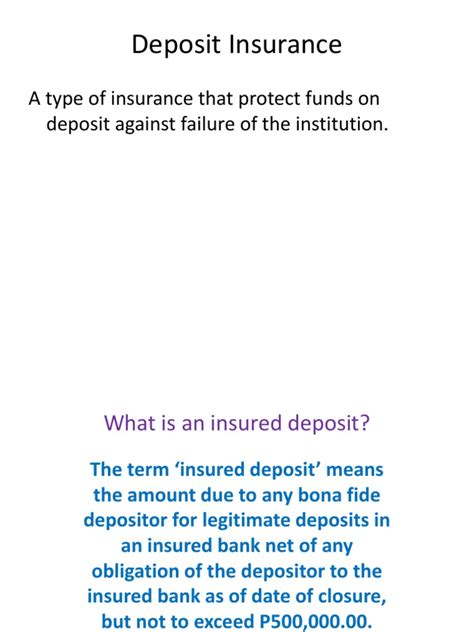

Deposit insurance is a protective measure designed to safeguard bank depositors by guaranteeing the safety of their funds up to a certain limit if the bank fails. It works by providing a government-backed or authorized agency guarantee that reimburses depositors in case their financial institution becomes insolvent or unable to fulfill withdrawal requests.

This insurance encourages confidence in the banking system, preventing bank runs during economic uncertainty. When a bank collapses, the deposit insurance agency steps in to compensate depositors up to the insured amount, typically covering savings, checking accounts, and certificates of deposit.

However, not all accounts or investments are covered, so understanding the specific terms and limits of deposit insurance is crucial for protecting personal finances effectively.

The Role of Government in Deposit Protection

Government plays a crucial role in safeguarding depositors’ funds, acting as a stabilizing force in the financial system. By implementing deposit protection schemes, it ensures that individuals and businesses maintain trust in banks even during economic turbulence.

This protection prevents panic withdrawals, which can lead to bank failures and wider financial crises. Governments establish clear regulations and fund insurance mechanisms that cover deposits up to a certain limit, shielding small savers from losses.

Beyond financial security, this role reinforces overall economic stability and consumer confidence, encouraging savings and investments. In essence, the government’s intervention not only protects individual assets but also supports a resilient banking environment that benefits society as a whole.

Types of Accounts Covered by Deposit Insurance

Deposit insurance protects various types of accounts to ensure the safety of depositors' funds in case a bank fails. Primarily, it covers individual savings accounts, checking accounts, and money market deposit accounts, providing peace of mind to personal account holders.

Additionally, certificates of deposit (CDs) are insured, safeguarding fixed-term investments. Trust accounts and retirement accounts, such as Individual Retirement Accounts (IRAs), are also typically protected under deposit insurance schemes, offering security for long-term savings.

However, the coverage limits may vary depending on the country and the insurance program’s rules. Joint accounts are insured separately for each co-owner, increasing protection for multiple account holders.

Business accounts, including those for small enterprises, may also be covered, but it depends on the specific insurance policy. Overall, deposit insurance plays a crucial role in maintaining public confidence in the banking system by protecting a wide range of deposit accounts.

Deposit Insurance Limits Explained Clearly

Deposit insurance limits act as a safety net, protecting your money in banks if financial trouble strikes. These limits define the maximum amount guaranteed by the insurer, ensuring depositors won’t lose all their funds during a bank failure.

Typically set by government agencies, these protections offer peace of mind, encouraging people to save and invest without fear. However, it’s important to know your coverage caps because funds beyond the insured limit might not be recoverable.

Different countries and institutions have varying limits, so understanding where your money stands helps in making smart financial choices. This safeguard plays a crucial role in maintaining trust and stability in the banking system, preventing panic and promoting economic confidence.

How to Verify If Your Bank Is Insured

To verify if your bank is insured, start by checking whether it is a member of the Federal Deposit Insurance Corporation (FDIC) in the United States or the equivalent insurance body in your country. You can visit the official FDIC website and use their BankFind tool to search for your bank’s name, which will confirm if deposits are protected up to the insured limit.

Additionally, banks often display their insurance status on their websites or at their physical branches, so look for FDIC signs or certificates. If you're still unsure, contacting your bank directly and asking about their insurance coverage can provide clarity and peace of mind.

Differences Between FDIC and NCUA Insurance

FDIC and NCUA insurance both protect depositors’ money but serve different types of financial institutions. FDIC insurance covers deposits in banks, while NCUA insurance protects members of credit unions.

Both guarantee up to $250,000 per depositor, per institution, ensuring funds are safe if the institution fails. The main difference lies in the type of organizations they insure: FDIC is for banks and savings associations, whereas NCUA is specific to federally insured credit unions.

This distinction is important for consumers to understand when choosing where to deposit their money. Both agencies aim to promote confidence in the financial system by securing deposits, but they operate independently under different regulatory frameworks.

Steps to Take When Your Bank Fails

When your bank fails, the first step is to stay calm and gather all essential documents like account statements and identification. Immediately contact the bank’s customer service or visit their official website to understand the next steps and confirm the bank’s status.

Check if your deposits are insured by government agencies like the FDIC or equivalent in your country, which usually guarantees funds up to a certain limit. Notify your employer and update any automatic payments or direct deposits to avoid disruptions.

If the bank is taken over or merged with another institution, follow their guidelines for account access and fund retrieval. Keep a close eye on your accounts for any unusual activity, and consider opening an account at a stable bank to ensure your finances remain secure.

What Deposit Insurance Does Not Cover

Deposit insurance offers crucial protection for bank customers, but it has important limitations. It typically covers deposits such as savings accounts, checking accounts, and certificates of deposit, up to a certain limit.

However, it does not cover investments like mutual funds, stocks, bonds, or annuities, even if these are purchased from a bank. Additionally, deposit insurance does not protect against losses due to theft, fraud, or bank failures involving uninsured deposits.

It also excludes valuables kept in safe deposit boxes. Understanding what deposit insurance does not cover is essential for managing financial risks and ensuring that your money is protected appropriately through diversification and other safeguards.

Impact of Deposit Insurance on Financial Stability

Deposit insurance plays a crucial role in enhancing financial stability by protecting depositors' funds in the event of a bank failure, thereby reducing the risk of bank runs and fostering public confidence in the banking system.

By guaranteeing a certain amount of deposits, it mitigates panic withdrawals that can destabilize financial institutions and the broader economy. Additionally, deposit insurance encourages prudent risk management among banks by imposing regulatory oversight and requirements.

However, if not properly designed, it may lead to moral hazard, where banks engage in riskier behavior, assuming they are protected. Overall, a well-structured deposit insurance scheme promotes trust, reduces systemic risk, and supports the continuous functioning of financial markets, which is essential for economic growth and stability.

How Deposit Insurance Protects Small Depositors

Deposit insurance plays a crucial role in safeguarding small depositors by guaranteeing the safety of their funds in banks and financial institutions. When a bank faces insolvency or financial distress, deposit insurance ensures that depositors do not lose their money up to a certain insured limit.

This protection boosts public confidence in the banking system, encouraging small savers to keep their money in banks without fear of losing it. Additionally, deposit insurance helps maintain financial stability by preventing bank runs, where many customers withdraw their money simultaneously.

By covering the deposits of individuals and small businesses, this system acts as a safety net, reducing the risk of financial hardship for vulnerable depositors. Overall, deposit insurance is essential for promoting trust and stability within the economy, especially benefiting small depositors who rely heavily on their savings.

Ultimately

In conclusion, understanding whether your deposits are insured is crucial for protecting your hard-earned money and ensuring peace of mind. Always check the coverage limits and the institutions covered by deposit insurance in your country.

Staying informed helps you make smarter financial decisions and avoid unnecessary risks. Thank you for reading another interesting article, and don’t forget to share it with your friends! Goodbye!

Posting Komentar